The adult industry is seeing new and updated tools for managing and preventing chargebacks, with developments from major card networks and specialized platforms. These solutions aim to help businesses navigate compliance standards and reduce financial losses from disputes.

Industry Developments and Compliance

The year 2023 brought several significant changes affecting the industry. Visa lowered the limit on surcharging to 3%, and Mastercard updated its Business Risk Assessment and Mitigation (BRAM) program. The BRAM update affirmed that publishing images using someone’s likeness without their consent is not permitted. Artificial intelligence (AI) also continued its rapid growth, impacting various aspects of business operations.

Jonathan Corona, Chief Operating Officer of MobiusPay, has two decades of experience in the electronic payments processing industry. His responsibilities include reviewing and advising merchants on compliance standards mandated by card associations, such as BRAM guidelines and chargeback compliance rules defined in Visa and Mastercard operating regulations.

Businesses are encouraged to improve how they accept credit card payments and protect transactions. Steps to prevent chargebacks include implementing good billing practices, utilizing 3-D Secure, AVS, and CVV, and maintaining a liberal refund policy. Despite these measures, fraudsters continue to attempt to defraud businesses, and issuing banks often side with cardholders, particularly against adult businesses.

Chargeback Prevention and Resolution Tools

Several tools are available to help alleviate chargeback concerns. These include Rapid Dispute Resolution (RDR) and Cardholder Dispute Resolution Network (CDRN) by Visa, and Ethoca Alerts by Mastercard. These tools provide merchants with resources to intercept and prevent chargebacks, and have been particularly effective in adult and dating verticals, where they have significantly reduced chargeback ratios.

CDRN and Ethoca Alerts require human intervention, offering businesses 24-72 hours to take action. For tangible products, this time can be used to cancel or divert a shipment. For membership-based businesses, it provides an opportunity to contact the member. This allows businesses to issue a refund, address a consumer complaint, or investigate further, rather than encountering an unexpected chargeback.

RDR functions similarly to a chargeback but does not count towards a business’s chargeback ratio. It operates without human intervention, automatically debiting the transaction amount from the bank account. A key feature of RDR is the ability for business owners to create rules for how cases are handled. For example, a business might set a rule to automatically refund every case under $50, or to refund only specific chargeback reason codes. These services can be activated or deactivated as needed.

Order Insight, enhanced with Compelling Evidence 3.0 (CE3.0), is specific to Visa 10.4 disputes, which pertain to "fraud card-absent environment." CE3.0 provides transaction information directly to issuing banks to identify and block misuse of the chargeback system, contributing to lower chargeback ratios.

In 2026, Visa released six new or updated dispute-resolution services, a year after acquirers became subject to the Visa Acquirer Monitoring Program (VAMP). VAMP consolidated five fraud and dispute programs and reduced 38 distinct remediation processes into one program. Enrollment in VAMP begins when a merchant’s or acquirer’s VAMP ratio exceeds Visa’s limits. For merchants, this limit is 1.5%. Acquirers have two thresholds: an “excessive” one at 0.7% and “above standard” at 0.5%. Visa processed 106 million disputes globally in 2025, a 35% increase from 2019.

The new tools for acquirers include the incorporation of AI predictive models in the Dispute Intelligence tool, which Visa states should assist with analysis. Dispute Doc Analyzer uses AI to expedite processes, making it easier for acquirers to auto-populate questionnaires for merchants and providing summaries of merchant documents for issuers. The third new service for acquirers is Visa Dispute Case Manager, which also uses AI to simplify workflows in a centralized platform. The Dispute Intelligence tool and Dispute Doc Analyzer are currently available, while the Case Manager will be available in North America in 2026.

The Role of AI in Chargeback Management

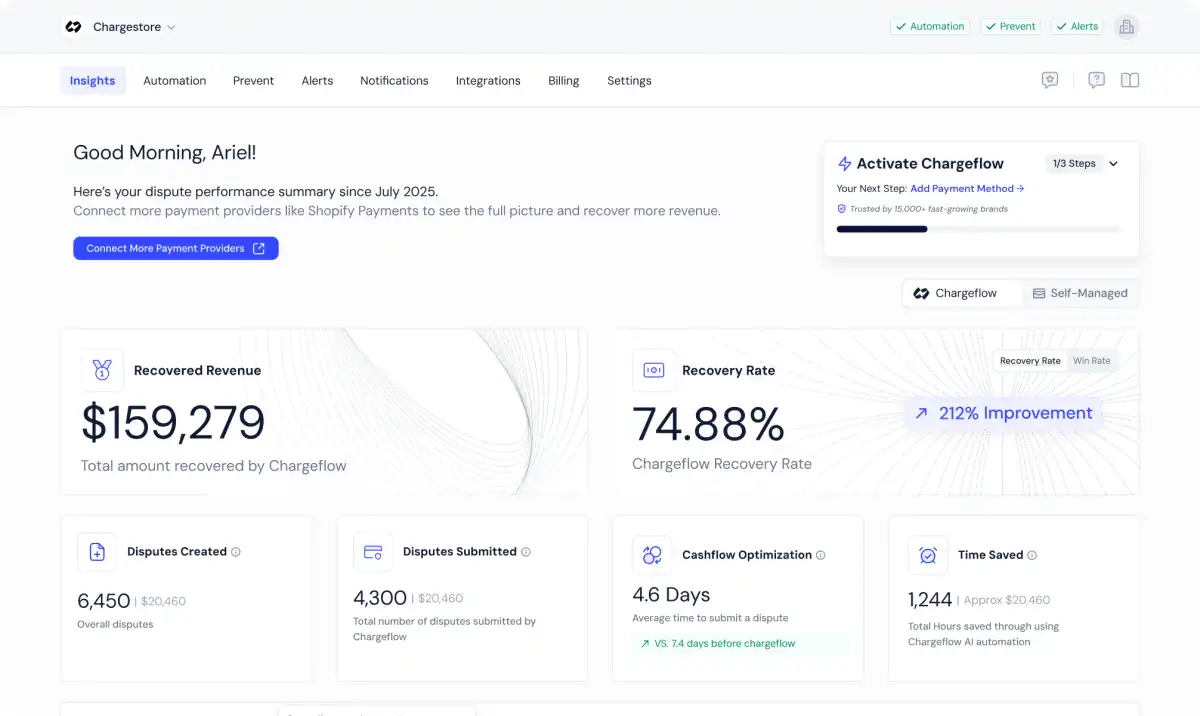

AI continues to play an increasing role in chargeback management. Chargeflow, for example, offers an AI Chargeback Platform designed to reduce dispute rates and maximize chargeback recovery. This platform leverages data from a global network of merchants to protect businesses against chargebacks. Chargeflow automates chargebacks and inquiries end-to-end, and its AI-driven technology combats fraudulent chargebacks. The platform supports over 100 integrations with payments, eCommerce, and CRM platforms. Chargeflow operates on a success-driven pricing model, charging only for recovered chargebacks, and offers a 4X ROI Guarantee. It also ensures a 100% submission rate, preventing missed chargeback deadlines, and allows for personalization, such as delaying submissions for internal review. Chargeflow also supports inquiry disputes in BNPL platforms.

ChargebackHelp offers services including Deflect, which aims to avert disputes by providing transaction data at the point of inquiry. Their Resolve service uses real-time alerts to address issues before they become chargebacks. Recover, their post-chargeback service, uses automated representment to reclaim revenue.

Key Facts

- Visa lowered the limit on surcharging to 3% in 2023.

- Mastercard updated its BRAM program in 2023, requiring consent for likeness use in images.

- Visa processed 106 million disputes globally in 2025, a 35% increase from 2019.

- New Visa tools for acquirers include AI-powered Dispute Intelligence, Dispute Doc Analyzer, and Visa Dispute Case Manager.

- Chargeflow offers an AI Chargeback Platform designed to reduce dispute rates and maximize chargeback recovery.

- Jonathan Corona of MobiusPay advises merchants on compliance standards, including BRAM guidelines and chargeback rules.